Planning Briefs

High Income Earners & Roth Conversion

Published Wednesday, November 28, 2018 at: 7:00 AM EST

Roth IRAs are tax-free, making them popular, but a married couple is ineligible to contribute to a Roth if they earned more than $199,000 of modified adjusted gross income in 2018 ($135,000, if single). A "backdoor" around this limit enables you to convert traditional IRA assets into tax-free Roth IRA accounts, even if you're over the income limit. Here's a strategic approach for maximizing the backdoor route to get tax-free Roth treatment with the least amount of conversion-tax.

When you convert a traditional IRA to a Roth account, you are required to pay tax on the income withdrawn from your traditional IRA. If you do not have the cash on hand to pay the extra income tax you'll owe next April 15, you probably should forget about converting now; withdrawing a larger sum to pay for the income taxes is a risky financial bet and is generally unwise.

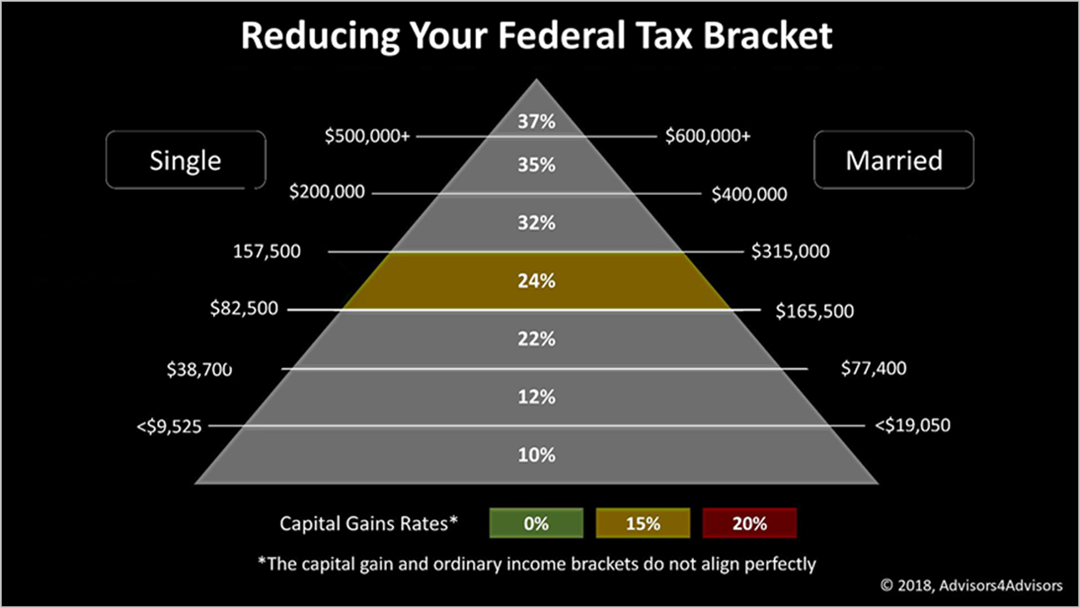

If you have the cash on hand to pay the extra income tax you'll owe in the year you draw from your traditional IRA to make the conversion to the Roth, your next move is maximizing your tax bracket. For instance, if your taxable income is $177,500 after making a $100,000 withdrawal from the traditional IRA, consider lowering the amount you convert to avoid pushing you into the 32% bracket. Reducing a $130,000 contribution to a Roth by $30,000 lowers your maximum tax bracket to 24%, for example, giving you the maximum benefit of the 24% bracket.

© 2024 Advisor Products Inc. All Rights Reserved.

More articles

- Time Itemized Deductions To Reduce Taxes

- The Big New Tax Break For Pre-Retired Professionals

- Sidestepping New Limits On Charitable Donations

- The Truth About U.S. GDP Growth

- Another Member Of Music Royalty Dies With No Will

- Paying Off A Mortgage And The New Tax Code

- Key Facts On Deducting Medical Expenses

- Reduce Your Widow's Tax Bill Materially Annually

- Ten Things About 10-Year U.S. Stock Market Performance

- Qualifying For The New Business Owner Tax Break

- Your Alma Mater Or Your Family?

- This Is Not Your Parents' Interest Rate Cycle

- If Family Is Wealth, Then Planning Is Immortality

- Life Is Fragile, So, Please, Value Each Day As Priceless

- Everything You've Learned About Interest Rates May Be Wrong